From Company's Prospectus

1. Business Operation

Independent oil and gas exploration

and production (E&P) company with a set of proprietary exploration

technologies (“Rex Technologies”). Scheduled to be listed on the Catalist, Rex is a small cap

independent oil and gas E&P company with a set of proprietary exploration

technologies - Rex Technologies. This is the 2nd E&P company listed on the

SGX after the recent stellar performance of Mainboard's KrisEnergy.

Rex Technologies

From Company's Prospectus

Developed by the founders. Rex Technologies were developed by the founders of Rex

Partners Ltd, Dr Karl Ligren and Mr Hans Lidgen, It comprises 3 key proprietary

and innovative exploration technologies: Rex Gravity, Rex Seepage and Rex

Virtual Drilling.

From Company's Prospectus

REX claims its high success ratio compared to the peers. According to the prospectus, Rex

Technologies were 100% accurate in its predictions based on the 18 external

tests conducted over the last 24 months. The worldwide success ratios in

exploration drilling using Rex Technologies is estimated to be in excess of

50%, and Rex's Directors are of the opinion that this is much higher than the

estimated average world wide and industry-wide success ratio of 10% to 15%. NOTE: Theoretically, this sound wonderful

and exciting. However, I have my doubt see 5. Investment Risk.

New Start up firm

with first production expected in 4Q13. Rex is a relatively young start up, incorporated only in

11 Jan 2013. Rex

recently commenced a 80-well onshore drilling in the United States (7May13) and

plans to drill two offshore wells in its Oman concession in late 2013 as well

as the first well in each of its other two offshore concessions in the Middle

East in 2014.

From Company's Prospectus

Geographically diversified

concessions at more stable regulatory regimes than KrisEnergy. Rex has a diversified geographic concession

in Middle East ,

Norway and USA

From Company's Prospectus

The table

below provides a detailed breakdown on its concession:

From Company's Prospectus

2. Use of Proceeds

From Company's Prospectus

Note: Most of the proceed

(S$36m) will be funded to its drilling expenses. It basically means

that you are betting on the company's ability to achieve high success rate in

its drilling.

3. Financial Highlights

Offering price of

S$0.50 represents 229.2% premium above the Net Tangible Asset (NTA). At an offering price of S$0.50,

investor are paying 229.2% premium above its NTA. Thus the huge premium is

equivalent to the growth potential you are paying for the company.

From Company's Prospectus

Offering price is 20%

higher to pre-IPO investor. From table below, the offering price is 20% higher to the

pre-IPO investors. I think this is fair given that they are taking more risk.

From Company's Prospectus

Don't expect dividend anytime soon.

Do note that Rex

is a new start up and investor should not expect any dividend within the foreseeable

future unless their production start stabilizing.

Financial Statements is similar to

a new start-up company. Nothing unusual on its financial statement. Pretty common for a new

start-up company.

From Company's Prospectus - Income Statement

From Company's Prospectus - Balance Sheet

From Company's Prospectus - Cash Flow

4. Investment Highlights

Pure growth play. Like I mention above, Rex is a pure

growth play. Unlike KrisEnergy which already has existing producing fields, Rex

only starts its first concession in May 2013. Thus basically you are betting on

the company ability to deliver on all its promises. This is really a case of

high risk, higher reward.

Geographic

diversified concession with stable regulatory regime. This is definitely one of the

highlight investing in this company. It has a geographic diversified

portfolio and they are all in stable regulatory regime. Thus you can be sure that

the company is not dealing with some dodgy 3rd world countries (the likes of some

Africa and Latam countries) whereby you are

exposed to high political risk.

Ability to enter into

partnership deals. Rex prides that they are able to

get into strong partnerships with strategic partners. Well, to a certain

extent, this is definitely a strength, given that being a new company, more

established guys are willing to believe in them to form a partnership deals.

Nevertheless, I don't think it is anything to shout about as they are not the

major oil & gas players (e.g. Exxon, Shell & etc).

From Company's Prospectus

5. Investment Risk

Rex Technologies

might be over-hyped. So

according to the Prospectus, it mentioned that Rex Technologies has a

higher-than-average success ratio and it delivered 100% accurate predictions

based on 18 external tests conducted over the last 24 months. Well unless you

believe that 18 is a big sample size, this type of so-called tests is always

subjected to statistical basis. So, unless they are able to give me a HUGE

sample size, I would not buy the number easily.

Why do an IPO if

their technology is so good and accurate? Again, this baffle me. If Rex is such a good growth

story, why IPO the company to raise equity. Recall your Finance 101, equity is

ALWAYS an expensive cost of capital. If the success ratio is so high, they

could easily project its cash flow and go to the bank to borrow debt. Debt is

cheaper and it will provide them with leverage too. By doing so and getting the

production online and stabilize, I believe they can get an even higher IPO

valuation!!

If I can think of that, why can't they. It makes me wonder

if it is because the banks don't buy their story that's why they come out to

issue equity.

Note: I need to disclaim a bit on this argument. It might sound a bit too

extreme, but at guaranteedrisk.blogspot.sg, I will do this. I think it is my

duty to point out all the risk factors. As per Murphy's law, anything that can

go wrong will go wrong.

Management lacks the

track record compared to KrisEnergy. With all due respect, I think the management are all great

and capable guys. It's not easy to IPO a company, I'm not even sure if I can even do that. But unlike the KrisEnergy guys, the Rex's management lacks the track

record. You should know I'm a firm believer

of good management. Thus, I will need to monitor and access them myself as

the time goes on to conclude on this.

6. Technical Analysis

On the

back of the stellar performance of KrisEnergy, I would say the bid for oil

& gas E&P guys might be good.

Nevertheless, the stabilizing manager this time round is not CLSA but UOB Kay Hian. Thus I think the technical bid for this company will only at most be fair.

7. Conclusion

The recent IPO action has been

doing pretty well and flippers should be in the money. (with the exception of OUE H-Trust which I was never a big fan for

flipping it, see my article below)

Thus, investors will ask if they should do a flip on Rex?

Personally, I will be staying away from it this time round.

My strategy is take a break and see how bullish & strong the IPO market

really is.

Nevertheless on a fundamental perspective, Rex represents a

high risk and higher return stock. If you believe the company can deliver on

their production level, go in and GRAB it. If not, it is safer to stay away

from such a risky investment.

Personally, at offer price of S$0.50, I will not be overly

excited. However, if it eventually drop to around the pre-IPO investors' level

of S$0.40, I might then go in

to add some. I'm targeting the S$0.40 level, as I believe this is the

"correct level" where the smart money (the pre-IPO guys) values the company.

Thus, just follow the smart money =)

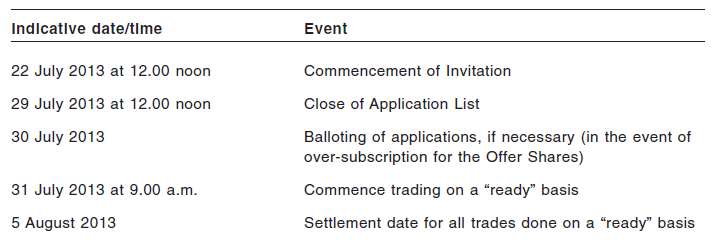

8. Timetable

From Company's Prospectus

No comments:

Post a Comment